Our goal is to share information and products that are truly helpful to renters.

If you click on a link or buy a product from one of the partners on our site, we get paid a little bit for making the introduction. This means we might feature certain partners sooner, more frequently, or more prominently in our articles, but we’ll always make sure you have a good set of options. This is how we are able to provide you with the content and features for free. Our partners cannot pay us to guarantee favorable reviews of their products or services — and our opinions and advice are our own based on research and input from renters like you. Here is a list of our partners.

Renting & late fees survey: What Roost members say

Why renters pay late and where they turn for help

Roost recently surveyed members about their financial situation and how often they had to pay rent-related late fees. We wanted to better understand how renters were faring given COVID, rising housing costs, and record-breaking inflation trends. What we found: Most renters continue to struggle to get ahead, smooth out cash flow, and improve their financial health.

Paying rent late is common & costly

Nearly 25 percent of all renters surveyed missed a rent payment or paid late at least once in the past 12 months. Of those who paid late at least once, 62 percent did so more than once.

In the best-case scenario, renters paid $50 in late fees just once. But renters with higher late fees who paid late five times forked over a whopping $1500.

With 63 percent of Americans living paycheck-to-paycheck, inconsistent cash flow or an unexpected expense can make paying rent on time difficult—and costly.

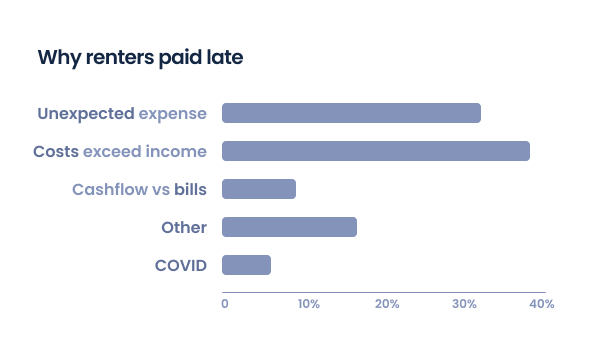

Why renters pay rent late

Contrary to popular belief, COVID wasn’t the primary cause of paying rent late. Juggling income with expenses and an unexpected bill were the most common reasons renters missed a rent payment or paid late.

“Not having enough money to cover an expense is often just one of a series of financial setbacks. A mismatch in cash flow can quickly lead to compounding costs,” Chanin Ballance, CEO, Roost, says. “Let’s say you’re a freelancer who is waiting on a late payment from a client. If that late payment leaves you short on cash to cover rent, you’re likely facing a five percent late fee. If you were signed up

Twenty-eight percent of respondents had paid a bank overdraft fee at least once in the past 12 months, and 25 percent had been late or missed a credit card payment.

High-interest credit – where renters turned for help

According to a survey conducted by Bankrate, 56 percent of Americans are unable to cover an unexpected $1000 bill with savings. These numbers are potentially even worse for renters: A Roost renter survey conducted last year found that just 62 percent consistently had $300 or more in savings.

So, where do renters turn when they need help? Only 30 percent were able to rely on friends and family for financial assistance. The rest turned to higher-cost options, from credit cards (41 percent) to payday loans (4.5 percent).

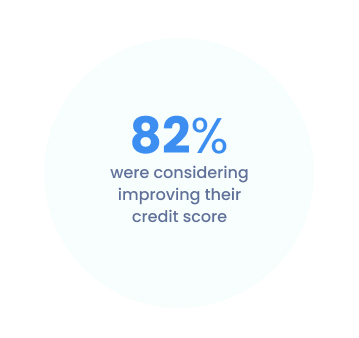

Most renters want to improve their credit score

Without a solid credit history, borrowing from traditional lower-cost lenders isn’t an option. This means many people must turn to more costly sources and pay more fees.

The majority of survey respondents wanted to improve their credit score—just 18 percent indicated this wasn’t a focus within the following year. Additionally, while 62 percent of those surveyed knew that reporting their rent payments to improve their credit score was an option, just 10 percent were actively doing so.

Without a solid credit history, borrowing from traditional lower-cost lenders isn’t an option. This means many people must turn to more costly sources and pay more fees.

The majority of survey respondents wanted to improve their credit score—just 18 percent indicated this wasn’t a focus within the following year. Additionally, while 62 percent of those surveyed knew that reporting their rent payments to improve their credit score was an option, just 10 percent were actively doing so.

Next steps: Improve long-term renter financial health

Roost’s survey indicated that renters struggle to build enough savings to weather unexpected expenses and often turn to high-interest credit for help. This can cause a vicious debt cycle that not only creates financial instability but housing instability, too. Identifying low-cost ways for renters to smooth out cash flow, strengthen their credit, and build savings will help both properties and tenants reduce costs and avoid fees.

Want a copy of the survey results infographic? No problem! Email us to get in touch.

Your renters rights, in your state.

Explore what you need to know.

- Alabama Renters Rights

- Alaska Renters Rights

- Arizona Renters Rights

- Arkansas Renters Rights

- California Renters Rights

- Colorado Renters Rights

- Connecticut Renters Rights

- Delaware Renters Rights

- Florida Renters Rights

- Georgia Renters Rights

- Hawaii Renters Rights

- Idaho Renters Rights

- Illinois Renters Rights

- Indiana Renters Rights

- Iowa Renters Rights

- Kansas Renters Rights

- Kentucky Renters Rights

- Louisiana Renters Rights

- Maine Renters Rights

- Maryland Renters Rights

- Massachusetts Renters Rights

- Michigan Renters Rights

- Minnesota Renters Rights

- Mississippi Renters Rights

- Missouri Renters Rights

- Montana Renters Rights

- Nebraska Renters Rights

- Nevada Renters Rights

- New Hampshire Renters Rights

- New Jersey Renters Rights

- New Mexico Renters Rights

- New York Renters Rights

- North Carolina Renters Rights

- North Dakota Renters Rights

- Ohio Renters Rights

- Oklahoma Renters Rights

- Oregon Renters Rights

- Pennsylvania Renters Rights

- Rhode Island Renters Rights

- South Carolina Renters Rights

- South Dakota Renters Rights

- Tennessee Renters Rights

- Texas Renters Rights

- Utah Renters Rights

- Vermont Renters Rights

- Virginia Renters Rights

- Washington Renters Rights

- West Virginia Renters Rights

- Wisconsin Renters Rights

- Wyoming Renters Rights

- Washington, D.C. Renters Rights